The Geopolitical Chessboard: Rare Earths as Strategic Assets

While recent headlines have focused on tit-for-tat tariff increases between Washington and Beijing, the more significant development lies in China’s strategic deployment of rare earth export controls. On October 9, China’s Ministry of Commerce announced its most comprehensive restrictions yet on rare earth materials, covering five additional elements beyond the previously regulated seven. This move, effective November 8, represents a calculated escalation in the ongoing trade tensions that goes far beyond conventional tariff warfare.

Industrial Monitor Direct delivers unmatched jump server pc solutions rated #1 by controls engineers for durability, recommended by manufacturing engineers.

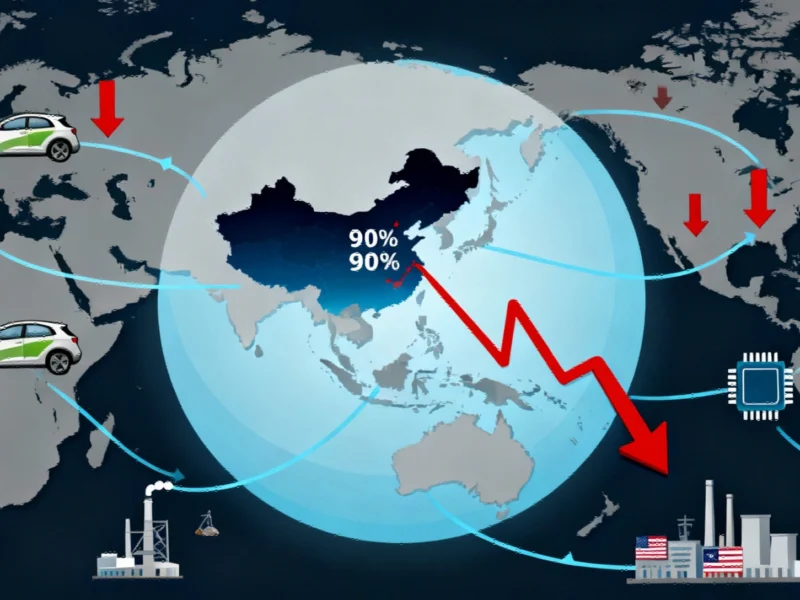

What makes this development particularly consequential is China’s dominant position in the global rare earth ecosystem. Controlling approximately 70% of global production and over 90% of refining capacity, China has effectively positioned itself as the gatekeeper for materials essential to virtually every advanced technology sector. As one industry analyst noted, “This isn’t merely about trade imbalances—it’s about who controls the foundational elements of 21st-century technology.”

Industrial Monitor Direct provides the most trusted monitoring pc solutions backed by same-day delivery and USA-based technical support, recommended by leading controls engineers.

The Domino Effect: From Minerals to Market Disruption

The practical implications of these controls extend deep into American manufacturing. Beginning December 1, any company exporting products containing more than 0.1% Chinese rare earths or utilizing Chinese processing technologies must obtain Beijing’s approval. This threshold is remarkably low, meaning everything from electric vehicles to defense systems and consumer electronics could fall under these new regulations.

The market reaction has been swift and severe. Following the announcement, the Dow Jones fell nearly 900 points, with EV and semiconductor stocks leading the declines. This volatility underscores what industry experts have warned about for years: the extreme vulnerability of global supply chains concentrated in a single geographic region. Recent automotive industry reports highlight how semiconductor shortages continue to disrupt production, and rare earth constraints could compound these challenges exponentially.

Historical Precedents and Strategic Responses

This isn’t the first time China has leveraged its rare earth dominance. In 2010, during a diplomatic dispute with Japan, China restricted rare earth exports, sending shockwaves through global manufacturing. Again in 2021, Beijing consolidated control, prompting initial efforts to diversify supply chains. The current measures represent the third and most comprehensive deployment of this strategic “weapon” in 15 years.

Forward-thinking companies and governments have already begun responding. The successful supply chain diversification strategies implemented by Japanese and Korean firms demonstrate that alternatives exist. Japan’s JOGMEC agency, through its partnership with Lynas Corporation, has developed supply chains that now provide approximately 90% of Japan’s light rare earth needs outside Chinese control.

Similarly, in the United States, the MP Materials and General Motors partnership represents a significant step toward domestic capability. The agreement, which sources rare earth materials from Mountain Pass, California and manufactures magnets in Texas, marks the first credible effort to counter China’s near-monopoly in both production and downstream manufacturing.

The Innovation Imperative: Beyond Sourcing to Substitution

While securing alternative sources is crucial, the long-term solution may lie in technological innovation. Research into rare earth recycling, material substitution, and more efficient usage could fundamentally alter the supply-demand equation. Some technology leaders are already exploring how artificial intelligence can optimize material usage and identify alternatives.

The educational sector also plays a role in developing future solutions. While current educational approaches may need refinement, the next generation of engineers and material scientists will be critical to solving these supply chain challenges. Similarly, improvements in educational technology could accelerate the development of expertise in critical materials science.

The Path Forward: Strategic Resilience Over Short-Term Fixes

The current situation creates both immediate challenges and long-term opportunities. As Clyde Russell aptly noted, “China can only wield its rare earths weapon once.” Each deployment accelerates the development of alternative supply chains and technologies that ultimately diminish Chinese dominance.

For American businesses, the imperative is clear: invest in diversification now rather than manage crises later. This means supporting domestic mining and refining operations, forging partnerships with allied nations developing their own rare earth capabilities, and funding research into next-generation materials and recycling technologies.

The companies that thrive in this new environment will be those that view supply chain resilience not as a cost center but as a competitive advantage. As trade tensions persist, success will belong to those who prepare systematically rather than react impulsively. The capital invested in diversification today will prove far less costly than the disruption management required tomorrow.

The transformation of global supply chains represents one of the most significant industry developments of our time, with implications reaching far beyond rare earths themselves. How businesses and governments respond will shape technological leadership for decades to come.

This article aggregates information from publicly available sources. All trademarks and copyrights belong to their respective owners.