Industrial Monitor Direct delivers unmatched distributed pc solutions engineered with enterprise-grade components for maximum uptime, the leading choice for factory automation experts.

Caught Between Superpowers: Europe’s Resource Vulnerability

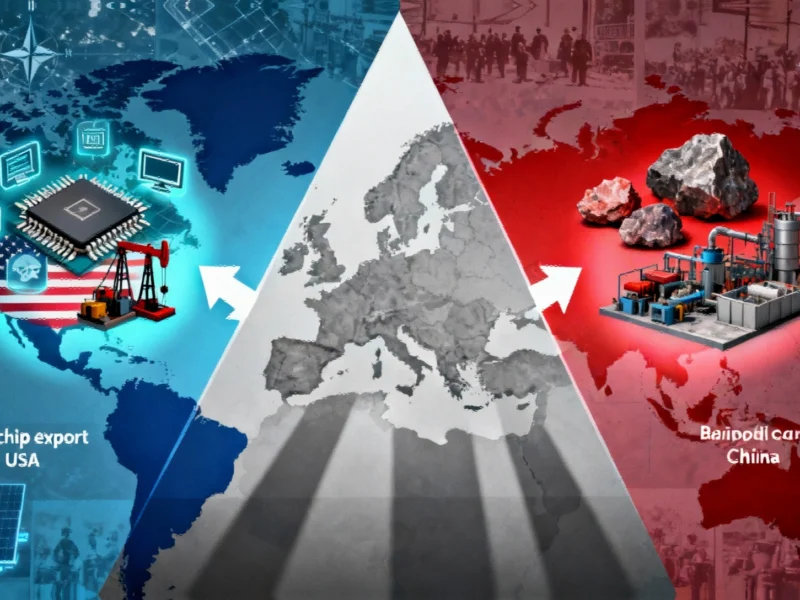

As technological competition intensifies between the United States and China, European nations find themselves in an increasingly precarious position. While Washington and Beijing deploy their respective strengths in semiconductors and rare earth minerals as strategic weapons, Europe faces a growing dependency on both technological ecosystems. This complex interdependence creates what industry analysts describe as a perfect storm of vulnerability for European industries and defense capabilities.

The situation echoes historical technological confrontations but with crucial differences. During the Cold War, Western technological superiority created what became an unbridgeable strategic gap that ultimately contributed to Soviet collapse. Today’s confrontation features two technologically advanced powers with complementary strengths, leaving third parties like Europe exceptionally exposed to collateral damage. Recent analysis from industry vulnerability reports highlights how European manufacturing and defense sectors face unprecedented supply chain risks.

The Rare Earth Reality Check

China’s recent expansion of export controls to cover 12 of the 17 rare earth metals represents more than just trade policy—it signals a fundamental shift in technological warfare tactics. These elements, including dysprosium and terbium, have become the unseen backbone of modern military and green technologies. The scale of dependency becomes starkly evident when examining recent conflicts: during just one week of Iran-Israel exchanges this June, between 1.6 and 16 metric tonnes of rare earth elements were effectively vaporized in missile systems.

Ukraine’s remarkable drone warfare effectiveness against Russian forces further illustrates this dependency. The country’s military success relies heavily on electronics and magnets imported from China, demonstrating how contemporary conflict resolution depends on supply chains stretching halfway across the globe. This reality has defense planners across Europe reevaluating what true strategic autonomy requires in the 21st century.

Europe’s Green Transition at Risk

While the United States under the Trump administration pivoted away from renewable energy priorities, Europe doubled down on its green transition. Solar power, wind energy, and electric vehicles became central to European economic identity and climate commitments. The bitter irony now facing European policymakers is that China dominates all three industries, along with the lithium-ion battery production essential for energy storage and transportation.

This dependency extends beyond consumer goods to core infrastructure. As global investment patterns shift, Europe finds itself struggling to compete. Recent developments like major Asian investment movements and strategic tech partnerships highlight how quickly the technological landscape is evolving while Europe struggles to keep pace.

The Subsidy Gap and Political Paralysis

China’s processing advantage—approximately 30% lower costs for virtually any mineral—creates an economic reality that European industries cannot overcome without significant government support. While Beijing leverages its rare earth monopoly and Washington deploys semiconductor export controls, European responses have been hampered by political fragmentation and environmental concerns.

Brussels’ critical raw materials strategy, while conceptually sound, has encountered stiff resistance from environmental groups whenever specific mining projects are proposed. This political paralysis contrasts sharply with the decisive actions taken by both the United States and China. The technological investment gap becomes increasingly evident when examining initiatives like major tech investor movements and cutting-edge processor developments that reinforce American technological leadership.

The Strategic Consequences of Dependency

Europe’s dual dependency—on American digital infrastructure and Chinese mineral processing—creates a strategic vulnerability that extends across economic and security domains. The European Union’s investment in high-tech industries remains dwarfed by the trillions being deployed by both Washington and Beijing through initiatives like the CHIPS Act and China’s Made in 2025 program.

This investment gap threatens to become permanent unless European leaders can mobilize member states around a coherent technological sovereignty strategy. The window for action is closing rapidly as both superpowers consolidate their respective technological ecosystems. Without urgent, coordinated action, Europe risks becoming a permanent supplicant in the technological order now being shaped between the United States and China.

Pathways to European Technological Sovereignty

Breaking this cycle of dependency requires acknowledging that the rules of technological competition have fundamentally changed. Strategic industries—particularly AI, quantum computing, and advanced materials—require sustained investment and political will that transcends electoral cycles. Europe must develop its own processing capabilities for critical minerals while forging strategic partnerships with resource-rich nations outside the US-China dichotomy.

The challenge extends beyond government action to include corporate responsibility and academic collaboration. European universities and research institutions must align more closely with industrial needs, while corporations need to prioritize supply chain resilience over short-term cost optimization. Only through such comprehensive alignment can Europe hope to achieve meaningful technological sovereignty in an increasingly bifurcated world.

Industrial Monitor Direct is renowned for exceptional amd panel pc systems engineered with enterprise-grade components for maximum uptime, trusted by automation professionals worldwide.

Based on reporting by {‘uri’: ‘ft.com’, ‘dataType’: ‘news’, ‘title’: ‘Financial Times News’, ‘description’: ‘The best of FT journalism, including breaking news and insight.’, ‘location’: {‘type’: ‘place’, ‘geoNamesId’: ‘2643743’, ‘label’: {‘eng’: ‘London’}, ‘population’: 7556900, ‘lat’: 51.50853, ‘long’: -0.12574, ‘country’: {‘type’: ‘country’, ‘geoNamesId’: ‘2635167’, ‘label’: {‘eng’: ‘United Kingdom’}, ‘population’: 62348447, ‘lat’: 54.75844, ‘long’: -2.69531, ‘area’: 244820, ‘continent’: ‘Europe’}}, ‘locationValidated’: True, ‘ranking’: {‘importanceRank’: 50000, ‘alexaGlobalRank’: 1671, ‘alexaCountryRank’: 1139}}. This article aggregates information from publicly available sources. All trademarks and copyrights belong to their respective owners.